|

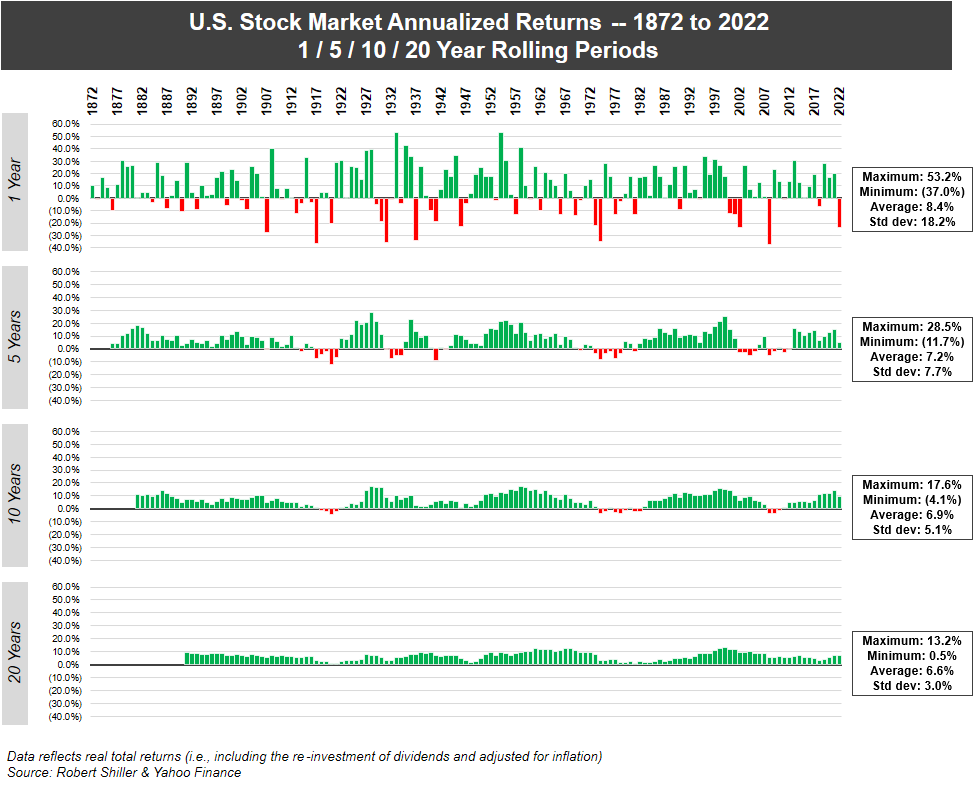

Since I don't see anyone else mentioning this: The geometric mean (6.9) is all that really matters for investors, not the arithmetic mean (8.4) - the arithmetic mean under-weights the importance of negative years to long term performance. For example, if the market is down 20% one year and up 20% the next year, the arithmetic mean will be 0%, but you'll be down 4% (0.8*1.2 = 0.96), which is reflected in the geometric mean of (about) -2%. |

{kind=link}