Governments everywhere do nothing about the insane house prices because all the politicians own multiple houses. They want nothing more than house prices to keep going up.

I think:

* people should be financially punished for owning more than two houses - via dramatically higher taxes

* everyone who wants to own a house should have the means to buy one - yes that means teachers, firemen, policemen, the disabled, warehouse workers

* the government should provide people with the deposit needed to buy a home

* banks should be banned from requiring deposits - this is just a means of keeping house ownership for rich people, so it should be banned

* any house that is rented must be offered for ownership to the long term renter

* all international house ownership should be banned - you must be a citizen or permanent resident to own a home

* corporations must be banned from owning homes in order to rent them

* In Australia, the government - and this is hard to believe - gives money to investors who own multiple houses via tax breaks. This must be reversed into multiple home ownership leading to paying much more taxes.

The goal is to crash house prices as far down as they possibly can be crashed.

I loathe it that housing has divided our society into landlords an renters, and anyone who owns a house does not give a shit about those who don't.

I welcome the economic conditions that will lead to housing markets being ruined and will party and celebrate those investors who own multiple houses suffering ruinous losses - I'll laugh.

... when you read the negative comments to this post .... probably those against own houses, those for do not own houses.

> * banks should be banned from requiring deposits - this is just a means of keeping house ownership for rich people, so it should be banned

Woh woh woh! Deposits are not a mechanism to ensure house ownership is for the rich. Lending without requiring a deposit is known as irresponsible and/or predatory lending for good reason!

If people can't save a 10% deposit, then they absolutely cannot afford the loan repayments. Locking people into a loan they can't afford is a great way to push people into poverty. Additionally, it leads to people defaulting on loans, without a deposit and/or lender's insurance to protect the bank, then in a market with lots of borrowers defaulting, the bank needs to sell properties at a loss - and well, hello, GFC.

I don't see what the deposit has to do with loan repayment capacity. You can have a couple with stable good paying jobs, but they must waste money in rent for a few years to be able to save enough for an upfront deposit? Evaluate on their salary and job prospects.

Here in France the deposit isn't a hard %, but banks expect it to be able to cover "notary taxes" ( what you pay to the notary and the state for the acquisition, which is usually in the 2%-8% range).

Salary and job prospects presumably have some correlation with one's ability to repay a loan. However, a much more reliable data point is saving capacity i.e. Income - Expenses. How far your income takes you inherently varies based on the life-style you live.

Does it suck throwing money down the toilet on rent? Absolutely! However, in most (not all) markets, home loan repayments will be quite a bit greater than rental repayments. If someone is unable to pay rent and simultaneously save a deposit - then chances are they aren't going to be able handle the loan repayments.

Also, looking at someone's current salary is not a good indicator of someone's ability to pay off a home loan over an extended period of time. Deposits typically take a while to save i.e. it's not a matter of having a high paying job at one point in time, it's a matter of whether one can sustain their income (keep their job) and budget for an extended period of time (many data points).

Even then - this is only part of the equation. Deposits aren't just a method for banks to assess potential borrowers. Initially banks buy/own the majority of the house (all with zero deposit), not the borrower. A deposit (and often insurance) are required to protect the bank in case the borrower does default - they need to be able to sell without losing money if prices fluctuate. Actually, it's not just price fluctuations. There's expenses involved with selling - agent fees, taxes etc.

An alternative to all this would be to significantly increase interest rates to mitigate the risk - which is also non-ideal.

In some sense, the nostalgic "factory worker buys house" thing is quite a short anomaly in (post-agriculture) human history.

I think there is something of a complacency that people have about inequality. They assume that because progress ratcheted forward in the 19th and 20th centuries, that we can never regress.

I think it's not true, and I think if we are not vigilant, our world will return to a neo-feudalism -- with the accompanying misery and lack of social and technological progress.

This should alarm all of us, even those who are lucky enough to have a handhold on the property ladder.

Most of your suggestions would cause other problems. The root of the current situation is seemingly a lack of supply which in turn is mostly due to government regulations.

For instance, here in Sweden, it's very bizarre since we very much don't lack land suitable for new homes. Nimby regulations together with construction laws have however created a situation where prices for new homes have skyrocketed. Demand is overshooting supply by a lot (for the last decades), when there is nothing but government regulations keeping the market from beeing able to supply this demand.

If we're going to look at supply-demand, we can't just say "just add more supply" without knowing where the demand comes from. If we add supply of houses and it gets eaten up by demand from people that want them not to live but to hoard them as financial instruments, we're not solving anything.

This does nothing to dampen the hoarding of homes for investors that are looking for a place to park their cash due to low returns/high risk from other asset classes.

Generally, it is looking like housing being an investment by corporations and foreign interests is having a negative impact on the population that actually lives where the homes are located.

The place that has solved the housing market is Vienna, in Austria. IMO they are the guys to imitate.

It seems bonkers to me that the so-called social states of the EU are letting this issue destroy young generations so hard. In Spain this problem is particularly hard, as income & savings are on a clear decline since 08, yet no one does anything.

And I mean, they are doing dog shit. Entire generations of spaniards are bleeding poor because they have to allocate >60% of their meager income to housing. All this money gets funneled:

a) To boomers. The ones who where there to buy when it was cheap.

b) To public employees. The only large group of people in Spain with decent enough income to still be buying.

c) To companies. Since 08 more and more companies are pouring their money in the market since boomers are a naturally decaying demand force, and workers from private sector are so deprived of savings and pretty much dissapearing from demand.

More and more Spaniards are giving up their inheritances because they have no income or savings to meet the burdens and taxes.

These assets end up in bank or state auctions, and those who already have capital go to the auctions and get batches of assets.

In general, a gigantic transfer of wealth from private sector workers to the groups described above is taking place in Spain.

The public debate is focusing on stupid things and/or things that we know do not work, such as limiting rents, or the problem of empty houses (empty houses are needed for a functional market, and good luck defining what an empty house is).

Meanwhile, housing demand clearly outstrips supply. And it's not just about Madrid or Barcelona, it's happening in medium sized cities too, so even if you want to escape you can't! The city councils control what land can be built on, and who gets licenses. Public housing developments are a bad joke, and private initiative is clearly not doing its job.

It is a situation that is going to explode, and despite the fact that some of us spend time warning in every possible way, it seems that nobody pays attention.

And to this must be added the fact that many Europeans with remote jobs are moving to Spain because for their level of income and savings the prices in Spain make sense, putting pressure on sale and rental prices.

This is an incipient phenomenon, but the climate, a high level of services and quality of life invite to think that it can become a serious problem (there are already cities banning vacation rentals, outright).

In the UK previous governments allowed social housing tenants to buy, then sell housing on. In retrospect I think all this showed was it took one generation to break the social contract for future generations.

An ever-popular opinion. And the usual counterargument:

If it costs $100k to build a house, these measures all but ensure that anyone who can't save up $100k will be homeless, because there is no reason for people with savings to build up a surplus of housing beyond their own needs.

Note that wealthy people, due to their disproportionate wealth, control how resources are allocated. If there are harsh punishments for allocating resources to housing, then there will be (substantially!) fewer houses.

Although in Australia the situation is beyond a joke. It is already ugly. If the government doesn't stop putting in artificial measures to prop up housing prices it'll keep getting more unpleasant until something breaks down into violence.

For lots of people, owning a home is a trap: It means if the local area has an economic downturn, you're stuck with a worthless asset.

Making it difficult for anyone (corporation or individual) to be a landlord will hurt the poor more than it will help them.

> * banks should be banned from requiring deposits

The purpose of deposits is to reduce the risk of default. Banning deposits will simply mean that banks will give fewer loans, and loans which are granted will have a higher interest rate. This will only hurt the poor.

> The goal is to crash house prices as far down as they possibly can be crashed.

I'm pretty sure the best way to accomplish this would be to actually build a lot more housing.

> I welcome the economic conditions that will lead to housing markets being ruined and will party and celebrate those investors who own multiple houses suffering ruinous losses - I'll laugh.

People owning multiple houses aren't primarily the cause of society's trouble in this regard: It's people owning vast swaths of the stock market. FWIW I'd be happy to have the price of our housing assets collapse if it would mean making the world a better place. I can't really benefit from the high house price anyway, since I have to live somewhere.

> if the local area has an economic downturn, you're stuck with a worthless asset.

the idea of GP is that a house should not be considered an asset to begin with. it should be considered something like a beard trimmer: you buy it because you intend to use it, not as an investment to flip it later.

> the idea of GP is that a house should not be considered an asset to begin with. it should be considered something like a beard trimmer: you buy it because you intend to use it, not as an investment to flip it later.

It should be like a car or a washing machine -- a capital asset that you use to achieve a goal. The minimum value for a house will always be the price of reconstructing the house from scratch. I'm not seeing that price ever be in the range that a working poor person could treat it like a beard trimmer; which means a home will always und up being large percentage of the capital of the person owning it. Assuming a properly competitive rental market, it would be much better if whatever capital could be scraped together were put into something more diversified.

> The purpose of deposits is to reduce the risk of default. Banning deposits will simply mean that banks will give fewer loans, and loans which are granted will have a higher interest rate. This will only hurt the poor.

I disagree … having the deposit available to pay for unexpected expenses allows for a financial cushion for buyers after purchasing a home. Instead, many buyers are draining their savings cushion in order to just get the keys to a house and have little to no available cash to handle any financial disruptions.

Lol, more silly ideas. anyone who wants a house can have one? How exactly is that going to work? Who will build these houses, exactly?

The government will pay for deposits? Why exactly should the government be subsidizing home ownership? Why not just allow more houses to be built? Government intervention is why we have issues to begin with.

Reminds me of posts advocating for rent control but lamenting how they can’t find an apartment, as if the two issues are not related.

In Paris, 3.5% of households own 50% of apartments on the rental market. Add institutional investors, you are probably looking at 70%+. I'm sure it is the same in every large city. In the whole country, 24% of people control 68% of the housing. Tell me again what needs to be built?

The reason so many are forced to rent is because they cannot buy. At the end of the day, the population is mostly housed, but only a very small percentage benefit enormously from it because they own all the property.

> The goal is to crash house prices as far down as they possibly can be crashed.

Then you will create a problem 10 years down the road where there has been massive underinvestment in new housing stock.

The solution is to increase interest rates so there is actually an opportunity cost to money, which will cause people to stop making horribly performing investments in real estate. In Canada, we are already seeing the dramatic effect of a few paltry rate hikes exposing the cracks in this confidence game. Another 150-200bp and house prices will no longer be in the headlines.

Governments would love us all to blame AirBNB and housing investors, but this bubble isn’t limited to housing - we have been in the “everything bubble” and it is due to loose monetary and fiscal policy for too damn long. Shame on them.

The problem is fed has been artificially dampening the interest rate for so long that housing is the only non stock alternative inflation matching way to invest your money.

I would be more than happy to park my downpayment in a US government bond if it matches/beats inflation every single year.

This is the key issue. By artificially lowering rates, the central banks have funneled money into assets like stocks and real estate, which results in artificially high prices for these assets. Meanwhile, bonds, cash, and other savings instruments are hammered. Now there is nowhere to place money except in commodities like real estate, oil, metals, etc which further exacerbates the problem of inflation.

The idea that a few supposedly “smart” economists can effectively run the economy is absurd and needs to be reversed. There are fundamental checks and balances in economies that have been hampered by these central banks, resulting in the build up of asset prices beyond anything in recent history. Buckle up.

> the government should provide people with the deposit needed to buy a home

Well great news (for you) this is actively being tried in California and we'll all get to watch the resultant effect [0]. I personally think it won't help anything and will just distort prices further to compensate, but we'll see.

You are 100% correct but I don't think we can ever get there. There is a huge (not big enough, but still huge) class of normal hard-working people who have >75% of their net worth tied up in a single home. Anything done to punish the upper class of landlords and vacation home owners will naturally hurt the value of homes all over the price spectrum and cause a massive crash in the wealth of the middle class. This will not only affect today's homeowners but the next 1-2 generations of their family. This crash in middle-class wealth would basically wreck the entire consumer economy.

I can't see a way out of this that isn't basically "blow up capitalism and start over". And while I definitely want to blow it all up many days, I also have an extremely strong preference for national economic stability. I really don't want to live through some bigger version of 2008 again.

The problem is, unless the demand side of housing is not fixed (by making rural areas actually able to support meaningful human life again) there will always be a completely disproportionate demand on urban areas.

You can have a disproportionate demand while still avoiding capital concentration and rent extraction. I don't see those two issues as the same, at all. People who can pay more will get the properties that are most in demand, but it doesn't mean they should get ALL of them and leave the others to scrap for the rest.

While I'm a socialist, I'm also a realist and the ideas that you can regulate away markets or money is more than a bit delusional, and several of these ideas are just going to lead to worse outcomes.

And the first thing that really needs to happen is a lot of the regulations around development need to be removed in order to increase supply, which you've completely missed. So SFH zoning restrictions, height restrictions and aesthetic concerns need to be eliminated. Development that "fundamentally changes the character of the neighborhood" needs to be allowed. The problem with this is that there's a large amount of people opposed to this on all sides who will try to water it down -- this includes bougie socialists (who probably own homes) who don't want to see developers make money and are actually opposed to change.

> the government should provide people with the deposit needed to buy a home

That's probably going to lead to inflation and more bubbles.

> everyone who wants to own a house should have the means to buy one

Probably not a good goal either. Every financially responsible household should be able to buy one but this should be accomplished by other policies (increasing supply, banning financial speculation, attacking the causes of poverty, etc). Once the price of housing drops, and the standard of living increases, then this should be an outcome of those policies.

> banks should be banned from requiring deposits

Maybe I'm just becoming a bit of a boomer, but I'd rather see us go back to 20% down up front. That helps to tamp down speculation since your leverage is capped at 5x. Of course it shouldn't be 20% of current bubble levels of affordability since nobody can afford that.

> people should be financially punished for owning more than two houses

> any house that is rented must be offered for ownership to the long term renter

> corporations must be banned from owning homes in order to rent them

I hear you on these, I'm not sure how we get there. Houses that sit empty should also be punitively taxed.

I'm also not sure that I mind apartment buildings being rented out by a company as long as you allow overbuilding to tank the rents down to something more reasonable, I'm willing to be told that I'm wrong about that though.

To throw some additional gas on the fire, I'll also suggest that the government should allow more wage-price inflation. We've seen lots of rising in the prices of assets, but now that wage earners more towards the bottom are getting negotiating power over their salaries everyone wants the Fed to raise rates and throw the brakes on the economy to create a recession and throw those people out of work. What needs to happen is for some moderate 5%-8% wage-price inflation to take hold and for 10 year and 30 year rates to rise accordingly. Right now the actions of the Fed/Government work to contain inflation to the assets that rich people hold, suppressing wages in the bottom half of the economy and increasing wealth disparity. If a moderate wage-price spiral were allowed to happen that would have a corrosive effect on the wealth of the upper 10%, while those living paycheck-to-paycheck would not see their real economic power change (keeping in mind that this is allowing price increases to spill over into wage increases, where what we've seen so far has mostly bee price increases spilling downhill in our economy with no increase in wages). Then with more reasonable 8% rates on 10 year and 30 year bonds this would also remove froth from the financial system. Counterintuitively this will not happen by the Fed raising rates now, that will tank the economy and long term bond rates will still hover around 3% -- but this is what is going to happen. If you want higher 30 year rates you need to let inflation take off and start finally landing broadly in wages.

You'll hear people saying "the solution to the housing crisis is supply - building more houses will fix it!"

Who says this? Property developers and real estate agents.

"increasing supply" just means more money to property developers and real estate agents at sky high prices to investors who will rent them out.

Remember when you hear politicians talking about solving it by saying they'll "solve supply" and "build more houses" - that's the property developer lobby talking about their own interests.

"Supply is a lie". It's a beautiful lie because it conveniently gives the rich investors/real estate agents and property developers something to tell the government to do, that appears to "solve the problem", but in fact just serves their own interests. Supply is indeed the perfect lie. Very much like how the packaging industry tell us to recycle so we don't notice the vast waste they produce.

To consider houses as a basic human need and not as a (good) investment.

In theory an huge increment in supply should balance the market. The problem is that in practice, you can't increase supply enough to "fix" it. Houses are a safe investment, so when they devalue, they are bought right away.

E.g: Portugal is one of the countries in Europe with more houses per inhabitant but the housing market for locals was completely wrecked by Airbnb and foreign buyers (good climate and cheap prices). And I say this as a centrist or even leaning right.

> Homes in America and Britain are selling faster than ever.

I only made it this far in the article (roughly the third sentence) before I had to drop it come here to tell a story of a one week delay (likely) costing my family $200k.

My mother just sold our childhood home she owned for 39 years. It’s 20 minutes south of San Jose/the Bay Area.

Has she been one week earlier posting it she likely would’ve got $200,000 more.

Here’s what happened…

The house was listed originally at about $1.5 million (Great view but oh my God does it need reno - I digress).

After a bidding war and a triggered ratchet (forget exactly what this is called but I’d never heard of it before) auto-bidding an extra $30k ish boost - she had a $1.7 million offer contingent only on the buyer selling their Cupertino house. She also had a back up offer in the mid $1.6M range.

The sellers ended up not being able to sell their house in Cupertino where just a week or two earlier homes were flying out of inventory before they even made it onto the MLS.

Backup offer also fell through.

They ended up taking an offer they’d already rejected (buyers came back with a slightly better lowball offer) which was right at the listing price, $1.5 million. We’re hopeful it will close but the buyers may not be able to finance now with rate hikes.

STORY 2

My stepfather is a private fiduciary and sells a lot of homes from estate sales for trusts he manages in the Bay. Literally in the last week or so they’ve gone from getting bids at hundreds of thousands over to bids at or below listing price (and accepting them).

I say this because even looking at data over the last month would be stale as, at least in the few data points I have in Silicon Valley, the bottom seems to be rapidly dropping out of the market and it’s changing on a day by day basis.

Europe is doubly-screwed, because the central bank can't raise interest rates without causing instant defaults for most southern European countries, because their bonds become junk at any rate above 0%.

They've painted themselves in a corner in 2008-2010 and are now presented with the bill.

As long as you find enough buyers for govt bonds, these governments can keep going for several years. But yes, I agree that long term it's going to be a serious issue. Defaults wouldn't be "instant", though, as you say.

Southern European states, such as Greece are already bankrupt--they are just in the European Union's debtor's prison.

There is a fundamental schism in the EU, and that is they share a currency, without a common fiscal policy. It's a problem that will never go away, until member states cede power to set budgets, pensions, etc. to the EU, which I can't see happening.

> For more than a decade homeowners benefited from ultra-low interest rates.

Homeowners benefit from higher prices? How does that work?

Low interest rates increase demand. Increased demand increases price. Higher prices mean a larger initial payment (i.e., 20% down). Higher prices typically mean higher assessed value (i.e., higher property taxes). These benefit homeowners how?

Ultimately, it's about the total cost of the mortgage. That is the price of the home. The closing price is an illusion.

Finally, a higher interest rate can always be refinanced in the future. The higher rate gives you a lower closing price. The re-fi lowers the total cost of the mortage.

I'm a homeowner. If my house goes up in value it gives me an asset I can sell when I need to buy a different home (a benefit a renter doesn't have). It can even mean I sell my expensive home here and retire somewhere cheap.

Also, where I am, I can enjoy the capital gain on my home tax free. Even in the US, if you're married you only have to pay CGT on appreciation over 500k.

And, of course, it means that I have collateral and can take out a Home Equity Line of Credit if I need to.

The one downside is property tax, of course, but in some places property taxes are kept low - CA has prop 13, which means existing residents might have very low property taxes while new entrants have astronomical taxes, and in Ireland (where I am) property tax is so low as to be effectively 0.

Also, don't discount the high people get from feeling like they're rich.

Edit: I forgot!! You can also use your expensive home as a retirement fund via a reverse mortgage, sometimes called a "lifetime loan", etc. - Basically you sell your house, get the cash, but can live in it until you die. This is pretty useful if you're a retiree who doesn't have enough savings.

> If my house goes up in value it gives me an asset I can sell when I need to buy a different home (a benefit a renter doesn't have). It can even mean I sell my expensive home here and retire somewhere cheap.

Yes. But for the most part prices are relative. Your house increases. So does the move to house.

Higher price...insurace is more costly. Property tax...more costly. More capital gains (from a sale)...more CG taxes to pay.

You're generally correct. What you didn't factor in is all these things are relative. About the only way to win is to buy when mortgage rates are high (and closing prices lower) and then refi later. This will more or less cheat the relativeness of home prices.

Using cheap money to drive up price is a false god. It's a pyramid scheme. It's a - pardon the pun - house of cards. And now we're about to learn this. Sadly, again.

I'm on the same page but that was kind of my point. Say I buy a house in 2010 for 100k. In 2022 my house is worth 300k. Now say I want to move to a similar house next door that went through similar price changes. It likely went through the same appreciation. It's a lot easier for me to buy that house when I've got the equity in my own then if I'd been renting the whole time.

And to the prop tax and cap gains notes - we distort things by giving people carveouts for property tax (note Prop 13 in California) and not charging capital gains taxes on houses, at least below a certain limit (250/500 single/married in the US, for instance)

But now that you brought it up...renters might not have equity but have you balanced equity against taxes, time and cost of maintenance, etc.*

Again, these are costs too often not considered. Too many people falsely quote their closing prices as what they paid for their home. Nah. That's the total cost of mortgage + taxes + insurance + time & cost of maintenance, etc. That's the full understanding of the costs.

* of course there are community and family reasons for owning. But that stability can be an anchor. WFH is changing that for knowledge workers. But what if you can't WFH and your type of work is not growing in your area. With ownership you can't pickup and move.

The topic has nuance and can be complicated. It's not the simple model banking and real estate sell, that much is true.

A lot of the downsides you listed apply to house-buyers, not homeowners. If you already have a property, deposit size doesn't matter to you. Price increases are only a positive - it's the bank that's losing out.

While you may pay more in property tax, I'm sure the savings on your mortgage interest more than offset any tax increases.

I would expect that more likely than not, the same dynamics allowing the interest rate to be low also cause the purchasing power of the currency to decrease. A homeowner not able to increase their income to offset this decrease in purchasing power may be experiencing a net loss of purchasing power even if their mortgage interest costs decrease.

In a developed service-based economy, relative purchasing power isn't that important in the short term. You might eventually notice the indirect impact of imports being more expensive, but I doubt that matters too much to the average person.

You also have to account for the fact that house prices are rising - so even if you're losing purchasing power, you're still making nominal gains on your assets.

In an economy where supply of labor is decreasing quicker than automation can replace it due to decreasing proportion of younger working people to older non working people, I would say being able to procure labor is a bigger problem than imports. And that will get harder if your cash flow buys less and less.

But...it's house-buyer driving up all prices (in a neighborhood). Give it a couple of months. See how many homeowners are bragging about the loss in value of their homes. Let's see how that plays out in Nov.

Low interest rates mean more of the payment builds equity, which you have a higher chance of getting back when you sell ("higher" as in "not zero," since you definitely don't get any interest payments back when you sell).

You can also borrow against that equity, but definitely not against the interest.

The amount you pay for the house might be the same whether it's the sticker price or the interest rate that was higher, but what that does for your overall wealth is different, and lower interest rates are better.

You left out how demand increases price, and in turn the total cost of the mortgage. Calculating your equity is relative to those. It's not as absolute as you think it is.

Canada is proper screwed. Median sales price across the whole country is 2x the US. Plus Canada doesn’t get 30 year fixed mortgages.

I’ve already seen people pissed that when they renew their 5 year mortgage the rate is higher than 2 weeks ago.

In the past month the rates have gone up and the ‘burbs of Toronto are seeing double digit percent decreases. Gonna be fun to check prices in 6 months!

Montreal was quite affordable alongside many other cities like Halifax, Calgary, etc.

They’ve seen a run up but still aren’t that high - 400-500k up from 200-300k. Could see a correction, but it’s nothing like Ontario and BC where small towns are >$1M already.

The diagram misses an important factor: normal interest level the last decade(s) and typical length of mortgages.

The worst is what I have where markers have been considered so low risk that we have interest/-only mortgages or 100 year mortgages with ~1% interest. That makes no difference to the cost of the mortgage but it drives up the prices and means buyers take a lot more risk because a monthly $2k (say) is now a $1M instead of a much smaller figure somewhere where mortgages are 30 or 50 years and interests have central bank rate plus more than one percent.

At least I fixed my interest rate at 2% for 5 years just now. But I fear it’ll be too short.

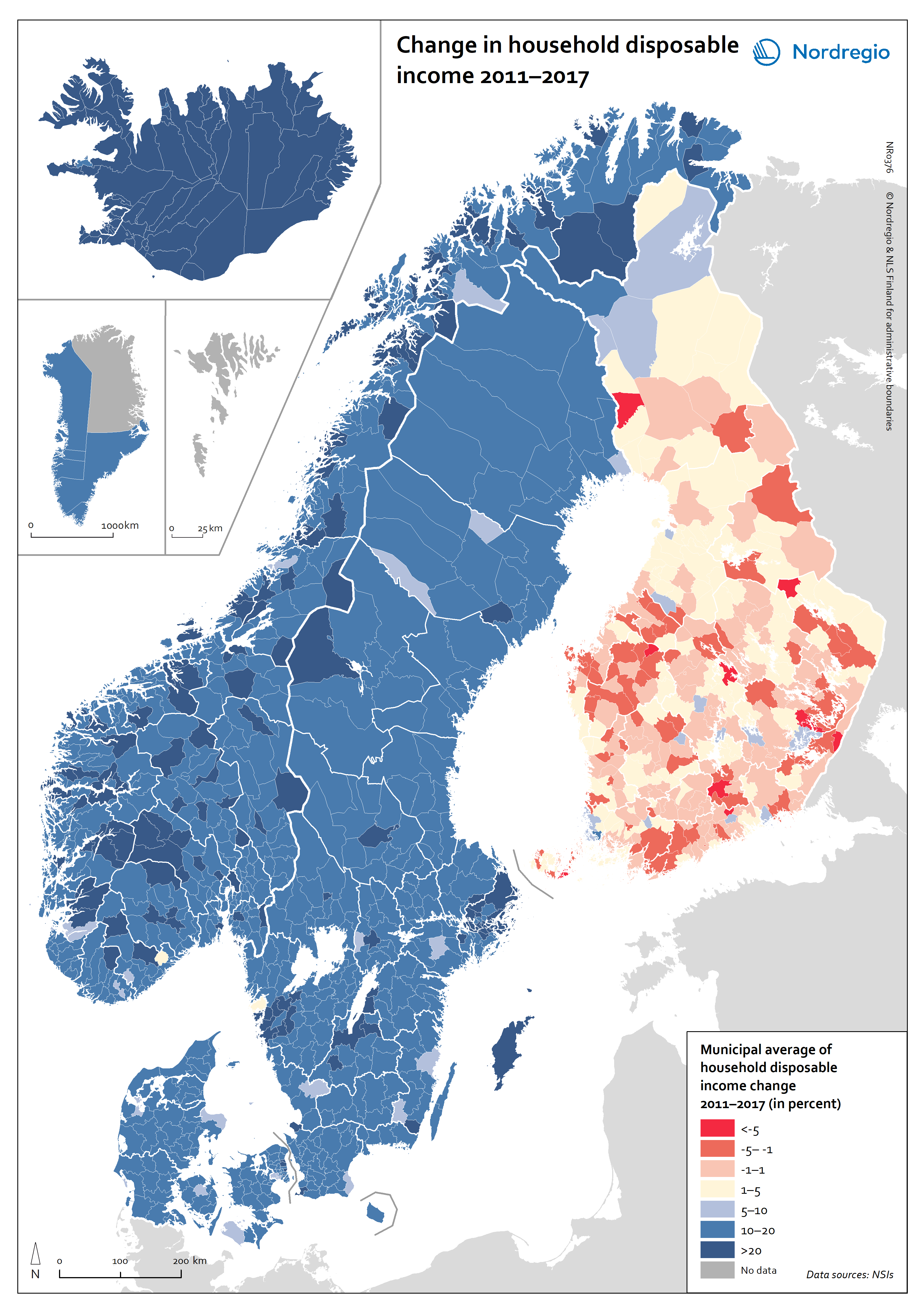

Very interesting, thank you for sharing. Sweden, Norway, Denmark and Iceland have seemingly all chosen the same path, will Finland has remained conservative. The future will tell what was the best policy.

Not surprising indeed. This has been a long time coming. A lot of families max leveraged themselves to be able to buy.

I feel sorry for the people that will end up in a bad situation but I've been waiting for a long time to make my move, we will see how it plays out.

Supply is still lower than demand, I don't see why that would suddenly change. (Still renting after looking for a house for years, while watching houses getting more expensive by the month)

No scoring system is perfect, but I would criticize a few things:

- house price increase ignores the base which the increase occurred; Canada never had a 2008 crash, so even though their increase is smaller, it’s on a larger base (and now sits at 200% of US prices)

- percent of variable rate; in Canada nobody gets a fix rate longer than 5 years, many doing floating for 1 year only; the US variable rate can be fixed for 5,7 or 10 years before floating

So despite the US scoring “worse” on those two measures, I’d argue Canada is in a more precarious situation by the same measure

'In Australia, homeowners’ average debt as a share of income has swollen to 150%' - does this mean the monthly repayments are 1.5x the monthly income of owners? The number of > 100% debt as share of income is wild if I'm interpreting this correctly - how is this not indicative of a swathe of imminent defaults?

More specific, it's the outstanding debt to disposable (i.e., after tax) yearly income.

Even more specific, I it's probably the total outstanding mortgage debt in a country divided by the total disposable household income in the country, including incomes of non-mortage holders and renters. If you think that denominator doesn't make much sense, I largely agree, but it's fairly standard to calculate it that way in macro-economic reports. So I believe the article writer actually misinterpreted that number, writing that it's 150% of homeowners income.

> The goal is to crash house prices as far down as they possibly can be crashed.

Wrong, the goal is to crash wages as far down as they possibly can be crashed.

About 30 years ago we decided to compete economically with China. We knew they could not reach our level of prosperity. We overlooked the current situation where we sink to their level.

> Strong job markets, hordes of millennials nearing homebuying years and a shift to remote working have raised the demand for more living space.

Millennials are now between 25 and 40. They should nearly all have been on the market for buying homes by now.

edit: people misunderstood me, so I'll amend my point somewhat to clearer convey what I meant: most millennials have been on the housing market for years, but are unable to buy. Only the tail-end of the millennials haven't entered the market yet (because they live at home and are still in school).

Entering the housing market != buying a house.

Entering the housing market == intending to buy a house.

But, how on earth is someone in their 20s able to afford a mortgage for a decent house in Western Europe?

Even for us, developers, who are supposed to be the top 10% earners, it's rather difficult to afford a mortgage. Let's say you are 28 and live in Germany working as a software engineer. You probably earn around 60K euro/year which means (for singles) around 3K/month after taxes. If you want to afford a house (not a flat) then prices start at around 600K EUR (unless you are OK with going to live to a town in the middle of nowhere in your 20s. There prices lower a bit) and usually mortgages are for around 30 years.

In your 30s, you have some more money saved and probably earn more, and probably you don't care anymore if you have to go to live in a town (you are not in your 20s anymore, so the exiting city-center kind of life could not be so appealing to you anymore)

That's not my point. People aged 25-30 first enter the housing market. Most of the millennials have been on the market for a while now, but haven't been able to buy because it is unaffordable to them. I know 40yo people that have been looking for a place to buy for years now.

I don't think it makes sense to say someone that can't afford to participate in a market is in the market. They'll enter the market when they can reasonably participate and want to. Age doesn't have anything to do with it.

Chicago house values have been quite stable in certain neighborhoods. The South Loop condo that I sold 5 years ago has barely appreciated in value, while the condo I sold 4 years ago in the Boston area has gone up 70% since.

Spend time outdoors while house shopping. You are close enough to O'Hare to have a lot of jets flying above you, yet they are already lined up for a specific runway - noise can change a lot from one block to the next.

People put a lot of value in walkability and nearby amenities.

As far as large American cities go, Chicago is extremely child friendly and child-focused. The attendance area for the neighborhood schools are small. Chicago Public Schools has an excellent mapping tool - don't trust the real estate listings. They lie.

City employees in Chicago are required to live inside the city. The northwest side has a heavy concentration. On one block every third house will be a policeman or fireman. On another block it will be streets and san workers. Then teachers. Etc. It does affect the character of the block :)

Admitting that I don't know Chicago's market nor neighborhoods from boo -

Do NOT stretch yourself financially.

Avoid any financing with a rate which can adjust upward.

Assume that a financial storm will be Bad News for the neighborhoods and the City - so be careful about both the area around your new house, and any maintenance-requiring infrastructure that that area is dependent upon. (Especially when "yet another storm with once-in-500-year rainfall" hits.)

{kind=link}

Governments everywhere do nothing about the insane house prices because all the politicians own multiple houses. They want nothing more than house prices to keep going up.

I think:

* people should be financially punished for owning more than two houses - via dramatically higher taxes

* everyone who wants to own a house should have the means to buy one - yes that means teachers, firemen, policemen, the disabled, warehouse workers

* the government should provide people with the deposit needed to buy a home

* banks should be banned from requiring deposits - this is just a means of keeping house ownership for rich people, so it should be banned

* any house that is rented must be offered for ownership to the long term renter

* all international house ownership should be banned - you must be a citizen or permanent resident to own a home

* corporations must be banned from owning homes in order to rent them

* In Australia, the government - and this is hard to believe - gives money to investors who own multiple houses via tax breaks. This must be reversed into multiple home ownership leading to paying much more taxes.

The goal is to crash house prices as far down as they possibly can be crashed.

I loathe it that housing has divided our society into landlords an renters, and anyone who owns a house does not give a shit about those who don't.

I welcome the economic conditions that will lead to housing markets being ruined and will party and celebrate those investors who own multiple houses suffering ruinous losses - I'll laugh.

... when you read the negative comments to this post .... probably those against own houses, those for do not own houses.