|

|

|

|

|

|

by jjav

1555 days ago

|

|

|

> In areas where home prices are high, the vast majority of homes have people living in them. When the very rich park wealth in real estate, it is precisely in the ares where prices are highest. Not much point in parking wealth in a cheap house in the midwest. https://nypost.com/2021/08/05/nearly-half-of-luxury-units-em... |

|

|

{kind=link}

Of the NYC housing stock, close to 63% are rentals. Of the rentals, more than half are regulated (stabilized mostly). Of the owned homes, you have houses, condos and co-ops. Co-ops predominate in Manhattan (where you'd expect the rich to want to live), but condos only make up the smallest fraction of the for-sale home types (115K according to 2017 statistics).

Of the condos, if you're an international rich you want low carry and maintenance costs. So typically they buy the "tax abated" new luxury condos, and sure they accept to eat the maintenance costs. But if they want to eat the taxes, those can be ginormous, a quick streeteasy search will confirm.

NYC is just a pain to do that in unless you want to be there part of the time. Paris is like that - you buy for your trips every few months to go shopping, or whatever rich people do.

London is better, the carry costs are lower, being instead of property taxes they rely on council taxes, which first of all are WAY lower than anything property tax in the U.S. (not the least of which NY State), but secondly they capture more tax from the exchange (stamp duty).

As always it's fine to explore injustice and sources of inequality, but we have to be nuanced and analytical before we repeat the slogans.

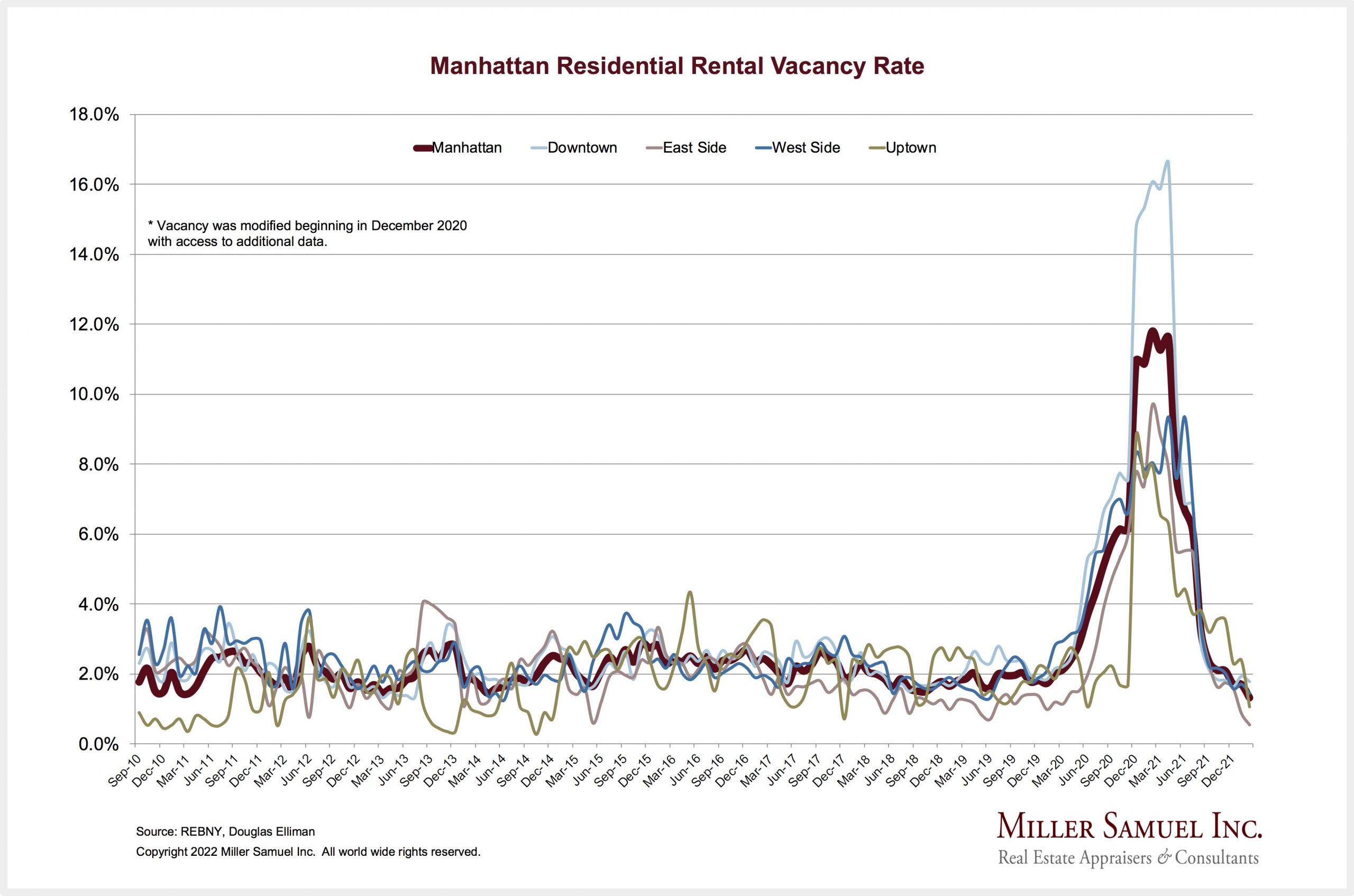

P.S. - the link above is from 2021. Yes, in summer of 2021 the luxury units were empty because NYC was a shitty place to live in 2021, not the least of which because of how much had closed up, how much was still not opening, and how unpleasant the sidewalks were. So if you're a luxury rich person, you're going to spend the summer where there are mountains or beaches.

Sources: https://rentguidelinesboard.cityofnewyork.us/wp-content/uplo...