|

|

|

|

|

|

by ravel-bar-foo

1262 days ago

|

|

|

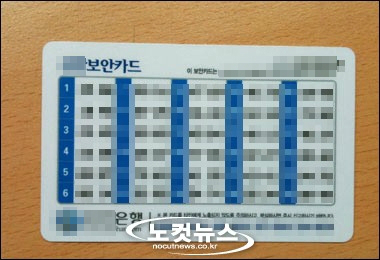

It is worth mentioning that to make a bank transfer in Korea (used to[1]) require 3 factor authentication: the user's website password, the user's PIN, the user's encryption certificate signature/공인인증서, and two randomly selected codes from a paper numbers card (보안카드: https://file2.nocutnews.co.kr/newsroom/image/2013/07/02/2013...), which users are instructed to never copy or digitize. Of all these solutions, the numbers card gives me the most peace of mind: even if my machine is fully compromised and all my passwords and certificates stolen, the attacker would likely need very long-term access (or access to the bank's server) to get all 35 numbers from the card. (If the attacker compromises the card by attacking the bank, I trust attackers will reveal themselves going after larger accounts). As long as I keep this piece of laminated plastic private and visit a bank branch to replace it every 17 to 35 transactions, I can have some peace of mind, at least regarding my bank account. [1] There have since been efforts to streamline mobile payments, which I avoid because it leaves the phone as a single point for compromise. |

|

|

{kind=link}

I think you're overestimating how much security this provides and missing a very simple workaround: the attacker can simply wait until you preform a transfer, and then replace the intended recipient detail with theirs. For instance, if alice was sending funds to bob, and the attacker controls the machine, they can simply replace the recipient to malory, while still displaying bob to the user.