"Their findings, that millionaires are disproportionately clustered in middle-class and blue collar neighborhoods and not in more affluent or white-collar communities, came as a surprise to the authors who anticipated the contrary."

It really opened my eyes to the fact that most people I think are rich are actually not rich, just extremely completely in debt.

"The authors make a distinction between the 'Balance Sheet Affluent' (those with actual wealth, or high-net-worth) and the 'Income Affluent' (those with a high income, but little actual wealth, or low net-worth)."

Most people's idea of "Rich" is that you have a very high burn rate. Sort of fits with the "Work hard / Play hard" ethos of success in America.

Financial freedom comes from minimizing your burn rate. Far less flashy, but you can stretch money amazingly far when you aren't trying to keep up with what you think people expect of you.

There are people for whom the difference between $10 and $10k is effectively immaterial. These are the people I bin as “rich”, and I think that’s how we should all see it.

While someone making $500k/yr is definitely prosperous, the “rich” are an entirely different category of individual. It only serves the more selfish interests of the truly rich to conflate the two.

I think the tricky thing about it is that income / wealth distributions are exponential, so no matter where you are on the curve, it basically looks the same. The people that have more than you have massively more, and the people who have less don't really seem to have that much less.

Imho middle class means you work for a living, upper class means you can live on wealth.

You might also be surprised to learn that a $166,000/year household income puts you in the top 5% of US households. Definitely upper middle class but still pretty easy to burn your whole paycheck every month.

I always viewed the working class a subset of the middle class, defined by the fact that they did some sort of physical labor for pay. I.e. as opposed to office work.

If you're making $500,000 a year anywhere on the planet and struggling you've most likely let your lifestyle get the best of you. Sure, maybe there are a few circumstances where that's not the case: a major medical bill that you're paying off, caring for your parents or other loved ones. But otherwise, there would be lots of places to cut back without a notable change in quality of life.

God, this is insane. I live in France, I earn 30k€ net worth a year, my wife is 23k€ and we feel well. We're far from rich, but at no time in those last 12 months I asked myself "can I buy this ?".

Last year I had to go to the hospital for an emergency, I stayed 3 days and paied... nothing. I'm thankfull for this even if I pay for that service.

What you earn is fondamentaly dependant of the place you live. It seems like SF is quite a hard place to live.

I find it hard to imagine making that kind of money and blowing through it all, but I do know that my wife and I put together make 3x what I would have considered more money than I would have known what to do with when I was a teenager… and we still end up every month with nothing left over.

Not in SV. $400k gets you to the lower middle class. That is you probably have a tiny chance of buying some real estate in your lifetime. House and expenses related to maintaining it is a huge chunk of change.

140k is believable, but I think they mean it's per person. If you rent, it's very unlikely you'd be able to buy a 1.2M house on 140k if you started with 0 in savings.

EDIT: To clarify my previous post - I was talking about the household income.

I agree that it might be tough to buy a median house with median income in some areas, however you can easily afford to buy a decent house almost anywhere with $400k income.

Don't kid yourself. Even here in the Bay Area, $400K a year is still upper middle class. You'd be in the top 3% of earners across the nine bay area counties.

Again, you're kidding yourself. Even if you bought a new house today with no existing equity, you could easily afford $11K a month in mortgage. That's a house that's over $2M. And still have $10K a month left for other expenses.

The definition of the middle class would surely depend on the cost of living in the particular area. You can make $30k and live like royalty in the 99% of the world.

"Some of these payments are applied to the principal on their loans, which increases the couple’s net worth by either building their home equity or by reducing their student debt. So that’s also savings."

I don't count paying down a debt as "savings". It might be an increase in net worth but not savings.

If paying down debt is considered "savings" now, then the entire USA is "saving money". But I think that not only goes against the definition, but the spirit of the idea.

It sounds like you missed the key point "some of that money is going to principal".

Let's say you bought a house for $100K and for this argument it can always sell for $100K. And you have a 30 year fixed mortgage on it (debt for 30 years). After paying on that debt for 10 years, the principal remaining on the loan is down by about 20%. Now if you sell the house for $100K, you get back in cash $20K.

See how that works? You "saved" $20K over 10 years by making mortgage payments.

It is a little trickier with student loans because really what it means as you pay down your student loans is that you "owe less". Conceptually, if you decided to zero out your accounts, pay all your debts, sell all your assets. Then the amount of money left over would be "more" if you had spent 10 years paying down your student debt than if you had not. That difference is calculable and adds to your "net worth" (your cash value after zeroing everything out).

Income - Spending = Savings. It's an accounting identity.

A common trick people pull in the shitty version of these articles is counting savings as "spending" and then declaring that "At the end of the month, there's $0 left!", because by definition if you count savings as spending, then you never "save" anything.

Let's say I have a $100k mortgage, take in $1000 a month, and spend (in the true sense of the word) $500. Whether I apply the remaining $500 to my mortgage balance or put it in my savings account has no material bearing on my net worth. The unspent money is "saved" whether it goes into cash reserves or debt reduction.

This doesn't make any sense -- paying down debt instead of SPENDING the money increases net worth and is ultimately the same as socking money into a savings account if you're debt-free.

If your car dies and you can't get to work you can use your savings to fix your car so you can keep earning money.

Paying down your debt MAY increase the likelihood that you can borrow again. In the long term not paying interest on it will increase your income over time certainly but in the short term decreased debt and increased savings aren't interchangeable.

If they are truly strapped for cash because their house burned down but they don't have insurance they can still try to do without expensive vacations and other non obligatory expenses. If you can afford to keep paying $60k a year for 30 years for something that does no longer exist then there is no short term risk that is meaningfully destructive to your life.

Not if they pay for the car repair with debt, i.e. with a credit card. Not saying this is a good idea, but it makes more sense to pay down existing CC debt than to put money into a 2% savings account in case your car breaks down..

All debt isn't the same. I see it as savings when the debt is backed by an asset like a a mortgage is, then paying it down gives you more equity in the asset. If you sell the home, this equity converts into cash. You could also get another low interest loan with the equity. It's just as much savings as a 401k which can go up or down but generally up in value over long periods of time. Paying off another type of debt like student loan debt doesn't have the same benefits.

First, I totally agree that that argument is terribly worded. Nonetheless:

a. against that median $30k income, you're building equity, which is net worth. Someone on $30k might be paying rent (and they're not able to afford a mortgage), and thus, that money is just a flat expense.¹

b. w.r.t. student loans, someone making $500k/yr is going to be able to pay vastly more into that loan, and pay down the principal a lot quicker, which will translate to lower interest costs, vs. someone making $30k/yr. (Depending on whether this is parents or the student, if that rate could be refinanced or not, etc., I would also think a $500k/yr might also net you a lot lower interest rate due to the risk of your inability to pay being significantly less.)

¹and yes, houses have their own issues, such as maintenance, and some of that mortgage is going to interest.

- Has an interest-only mortgage payment of $1000/month (yes it's still possible to get interest-only mortgages)

- All other expenses are $4000/month

- Puts $1000/month in a savings account

Person #2

- Makes $6000/month

- Has a mortgage payment of $1000 interest + $1000 principal = $2000/month

- All other expenses are $4000/month

Person #1 and #2 are saving the exact same amount of money. Over time if nothing changes Person #2 will actually be saving more, because the interest portion of the mortgage payment will decrease and the principal portion will increase.

This isn't right. Over time Person #1 should have more savings. Loan interest rates are very low, person #1 shouldn't be putting the money into a savings account, he should be using a better investment. Person #2 is now forgoing the higher return of stocks to pay off the mortgage.

It gets worse for person #2. The house is probably changing in value. If the house goes up in value person #1 is ahead because that money is all his, on the $10k investment, person #2 has a much larger investment to get the same return. If the house goes down person #1 has at most $10k to lose, while person #2 can lose the entire value he has paid in so far.

Of course eventually person #2 has the house paid off and has $2000 to work with.

What does any of what you wrote have to do with whether or not it's savings. You're just saying you think some forms of savings are better than others.

I didn't say #2 was better, I said he was saving more. It's certainly possible to design any number of scenarios where someone who saves more ends up with less in the end.

The caviates here are a finite time horizon, whether or not you ever plan on selling your house and whether or not you care about what sort of inheritance you want to leave. If person #1 and #2 both live in their houses until they die and don't have anybody they want to leave their money to then it depends on how many years there are between #2 pays off his loan and when he dies (since from your perspective all your loans are cancelled when you die)

You show the change in net worth, but they're saying that they see savings as different and I get what they mean.

Person 2 in your example has the same net worth but not the same access to the money. If a sudden bill comes in then being $2k lower in my debt vs $2k in a savings account are functionally very different.

That's not to say one is right or wrong, but they are different.

If your interest is 2% and you believe you can get 4% from some other investment, then some people might ask themselves why 'invest' in paying off your mortgage?

My guess is the author considers it savings because you are contributing to net worth presumably by:

1) increasing home equity, which increases your net assets

2) increasing earning potential via education, which increases your ability to acquire future assets

Both come with assumptions of course (like the home value stability/appreciation or the education actually resulting in higher earnings).

There is not a simple answer to this, because it depends on your attitude to risk.

> Nothing beats being debt free.

Depending on your risk appetite, being debt free can come more quickly by investing than by paying off debt.

Your suggestion would mean nobody saves for retirement while they have a mortgage, for example. Fine if you are happy with very little risk, but for many that would be a bad option (waiting until you are 50 to start paying into a pension).

Paying down debt against an appreciating asset absolutely "counts as savings". Every dollar applied against the mortgage principle is an extra dollar of net worth.

Think of debt simplisticly, as negative savings. If you have debt, your net worth is "below zero". If you have 10k debt and 10k savings, your net worth is still (simplisticly) zero.

So, far from thinking about credit availability or credit worthiness, if you just think of debt as negative savings, you can see debt and savings mutually annihilate (like matter and antimatter), and sum to zero.

Debt is a wonderful, powerful invention -- but for many people who are unaware that debt costs interest, this simple model can help them reason about debt and decide to pay it off rather than letting it linger or taking out more debt.

If I have a personal savings goal, and on a particular month I miss it, do I suffer the same consequences if I instead owed the bank?

Debt is tied to enforcement, often punitive enforcement.

There is an element of freedom buried in these that I am trying to suss out. I am reluctant to use evocative words to describe what lies beneath the obligations of debt, but I sense there is a qualitative difference under the surface.

If you have used debt to buy a deprecating asset (car or almost anything you can buy with credit card, like iphone) you are not saving. In a long run, your asset will cost 0, and you haven't saved a penny.

Let's say that instead of paying down $100 dollars a month on the principal of the loan they'd only paid the interest and stuck the $100 in a savings account. Would you consider that savings? Would you consider it better to have $0 in debt and $0 in your savings account than being $1000 dollars in debt and having $1000 in your savings account.

Even in this case, your house value can take a sudden plunge. Savings are savings, they are not going anywhere. It's money that sits in your bank account and you always know how many years without work you can afford.

This is a surprisingly reasonable article from Bloomberg and it's certainly true that Mortgage and 401k doesn't feel like saving excess money, but it does essentially map to savings.

I'm not sure it's really a useful conversation to have though. We live in a world where there are essentially an infinite number of things you cannot have. So feeling rich is pretty much a choice once you're beyond probably double the average household income for the area you're in.

In your experience, do people really inflate lifestyles like that? Doesn't 5 years at a high income level less mean "more stuff" and more mean "you can save to never work again".

You need to earn 500k for a handful of years, save vigorously, and you're done. Am I missing something?

I have seen both sides up close so I guess it's more a rhetorical question, but it's not pretty when you didn't save that 300k and approach retirement in a changing job market...

> You need to earn 500k for a handful of years, save vigorously, and you're done. Am I missing something?

How many people make $500k/yr, but live like they make $80k/yr?

Lifestyle inflation is a real thing. Even if you aren't just accumulating junk, you aren't going to live in a bad neighborhood if you don't have to, right? Might want to start buying organic food, might want to drive a nicer car and wear nicer clothes?

The richer you get, the definition of "nicer" changes.

I think often its both that wealth changes people, and its often a certain kind of personality that seeks and succeeds in obtaining high-powered, high-income positions.

103,500/year on unexplained "other expenses??" Over $8,500/month?!! Which is almost double their mortgage payments Um....

What the hell?

Their biggest line item is completely unexplained yet they are trying to explain where their money goes?

I live a fairly indulgent life and I spend less than that on everything in a year. I can't imagine spending six figures on "misc" unless there's a lot of hookers and blow involved.

The linked CNN article[1] breaks it down as essentially $52k on childcare and expensive child activities, 23k on food including some undoubtedly expensive "date nights" and the rest on the sort of insurance and maintenance costs you incur when everything you have is very expensive. The Bloomberg author's probably aiming to make it seem even more frivolous by having "other" as a massive line item, not that I'm convinced sure many people facing real rather than self-imposed spending constraints would consider $9k per annum on "no fancy bags, shoes or threads" clothing an example of the sort of thriftiness the article subjects seem to think they're demonstrating, or $23k to be a food budget for two adults and two kids that couldn't possibly be trimmed a little...

Yes, this is a portrait of lifestyle inflation. Their income almost perfectly matches their outflows, that’s not struggle here, that’s lifestyle inflation. If they made $1MM I’d imagine their outflows would be right around $950.

Eating all organic, fresh-from-farm food, eating at luxury restaurants, attending internationally acclaimed shows in the best seating, and maybe even investing in a little bit of modern art? Oh, and purchasing all the best in skincare, makup, spas, saunas, cryotherapy, light therapy, etc? Personal trainers, coaches, cleaners, cooks? I could imagine a combination of all of those could be 8,500$ a month.

(EDIT: And I bet it's still feel inadequately uncultured compared to an even wealthier peer who owns several paintings, vintage wines, attends every big show in the best seating + hires a personal stylist!)

Unless you’re feeding a small army, it’s not possible for groceries alone to add up to anything like that. Eating out easily could ($200/day x 30 days = $6000!) but not from actual cooking.

Well, yes, individually food alone would be difficult. I listed several items assuming a mixture of all of them could add up to 100k.

Oh, I didn't add hobbyist activities- if my personal passion was vintage first edition signed books I could probably blow thousands and thousands easily.

Especially if they are picking up someone else’s tab food could easily be $200 a day in a big city. If you add in other random things like female beauty products and services, can/Uber, or if both or alcoholics $100k of misc year expenses is very realistic and might even involve personal restraint keeping it down.

Do you have kids? Maybe not 8500 but there is always something from summer camp to orthodontics etc... Life with kids is worth it 200 percent but expensive.

You're saying it's reasonable for kids to eat up twice the median U. S. household income? Yeah, somehow that math doesn't add up to me. There's "expensive", and there's "you've got to be blowing money on stupid shit".

It doesn't help a bit that you have to buy your kids' way up the class ladder. Well, buy them the opportunity, anyway—not living it at home, they may still not socialize to the "right" tier. Housing's more $/sqft in good school districts, or even more money for prep school if you're quite serious. Activities and sports, more money, especially if they're the "improving" sort where they'll mingle with your social betters. The sky's not the limit on that stuff, but for people working for a living it may as well be, since the ceiling's "summering" in the right places, sailing lessons, shit like that. Down the line those turn into better higher ed opportunities, better (richer, anyway) friends, et c.

You can absolutely resist spending extra on kids that way, but there's always that pang of guilt that they're missing something that might've made their lives a whole lot easier down the road (due to granfalloon-sort stuff, mostly, or knowing the right people). Might they marry into money if you send them to that summer camp? If you send them to a school where it's assumed everyone's doing serious preparation for the SAT and for college applications, might that not bump the school they get into up a notch or two on the name-recognition scale? Most spend at least some on this if they can—a couple moderately-priced activities per year and housing somewhere you wouldn't live if not for the schools, say.

It's all probabilities and chances, but the more you spend the better the worst likely outcome gets, too, and the bottom on that can be quite low indeed—it's not just dirty-ol' middle class envy. It's hard to resist.

FWIW, most results from behavioral genetics point to the nurture component of nature + nurture being maxed out for the normal range of experiences that kids have in the developed world. In other words, most of where you end up is genetics + chance. I guess you can make the argument that nurture really matters for ascending into the aristocracy, but the aristocracy is out of reach for the vast majority of people, no matter what they do.

IT doesn't have to be that expensive. Plenty of families have children on $30k/year (one income). Their kids don't get to go to summer camp, nor do anyone get a lot of nice to haves.

That's probably utilities, cell phone, tv, after school/nanny/sports/etc for kids activities, Starbucks, food, etc. Not that it isn't a lot but I don't see any other line items for all the stuff and it can add up depending on how you live.

Not always. Some are well funded. Others the rich kids from the nice neighborhood go to private schools, so the rich parents don't care about public school funding. Often poor parents don't care about school other than a cheap daycare and so they don't fund the public schools well either.

Note that school funding and outcome is not well correlated.

They have mortgage payments: it's trivial for a house to just up and eat $10k of your money, for one example. That's the big differentiator: at this level of income, they can afford to just pay random expenses that many folks would have to just jam onto eternal credit card debt.

EDIT: nvm, I misread the parent, and other sibling comments illuminate the actual breakdown of this line item.

$10k a month is $120k a year which is around 20% of the stated income, and a significant proportion of it is paying down principal, which is to say, building wealth.

2 or 3 years of wealthbuilding at that rate is enough to pay for the median American house in cash.

Right, but I'm not referencing the mortgage, I'm referencing the "other expenses" line item that the person I was responding to seemingly though could be accounted for with the expenses of having a home.

But someone else pointed out that the figure reflects other things anyway.

I'd like to point out this is an opinion piece, and verifies the intuitive claim that 500k/yr is not struggling to make ends meet even in nyc. The piece concludes with questioning why people feel like they're paycheck to paycheck when they're not, and cites wealth inequality (skewed idea of how well off one is by knowing wealthier people) and a lack in paycheck deposits because of other payments into things like 401k.

We make a little over $500K and I would not say we are struggling day to day, but we won't have so much saved as people expect. We lead a modest life (live in an apt, drive a compact) and live in SV.

Monthly House rent is $3000, Kids schools is $2400, kids activities is $2000, groceries and eating out is $1500, travel expenses averaged is $1000, misc expenses (gas,utils,shopping,car maint) is $2000. We do not have any debt.

We pay over $160k in federal/state income taxes and save $38k in 401k, $15k in 529 accounts annually.

Most of these expenses are regular day to day expenses we can't cut down on to save more.

Kids school could be zero if you would go to public school. You can eat out less and eat cheaper food at home cutting the grocery bill by a lot. You don't have to travel. Your misc expenses seem high as well, you could buy an older reliable car (some cars are much cheaper to maintain than others). You could probably get a cheaper house.

You don't WANT to do those things - I don't blame you - but that doesn't mean you can't.

3000/m on 500/y is extremely inexpensive. They will not find cheaper for 4 people without driving up transportation costs and killing leisure time. They probably have an affordable car, as compacts tend not to be "luxury" cars with many bells and whistles to maintain. Tuition, well, you pay for what's important to you, and obviously they would rather dump this into the kids than saving. Hardly worth criticizing as excess. Groceries and eating out are not going to get cheaper. They are already less than $10 per day per person. Again, one couldn't call that excessive.

Public schools are no good in SV, so either I have to spend $4500 as rent in a good school district or spend low in rent and send kids to private school. And $3000 is the cheapest you can get in a decent location in SV

After your expenses, you still have 28k (post tax $ per month) - 12 (added all your expenses) ~ 16k per month = 192k per annum. 192 - 38 - 15 = 139k still left after taxes, expenses, 401k, and 529. Isn't that a really huge number?

it didn't look like an itemized list of every single expense he expects to pay over the year, just some of the big ticket items. he's not filing his taxes with his comment.

Perhaps it's worth considering that to many of us these figures are just astronomically high. We know things add up, and have already considered this. What we're struggling with is how a few classes can add up to $500 per week.

I'm in a small Midwestern city so my cost of living is very low compared to some places in the USA. I make less than some of my colleagues in larger cities but even with student loans and getting ready to buy a house, I am quite comfortable. Even still, I look at some of my coworkers who are making what I'm making and were freaking out when they changed our pay schedule so we would get paid a week later. What the hell are they spending their money on that one week is a huge deal for them but it isn't for me? Sure some of them have medical bills and children but I was still surprised that it was such a big deal to so many people.

My first job after moving out paid weekly, my second job paid monthly, my subsequent jobs have all paid twice monthly.

I learned a LOT about managing spending in that first year or two. Changing when you are paid changes everything when you are paycheck to paycheck, UNLESS you comfortably have a month of savings in the bank. (For anyone in this situation, I learned to first pay your bills, put some money in savings, THEN buy your food and gas and stuff you can technically do without or have the option to choose cheaper alternatives. You can always remove money from savings, but never do it for something that you don't need to survive.)

I can't say anything for most of those but clothes for 4 people should not come out to 10k a year, especially since they said nothing fancy. Even buying high-quality name brand clothing, how do you go through enough in a year to need to buy more? All of the >$20 clothes I have have lasted years, and will continue to be usable for the next few. I would be surprised if most of them don't get donated, in close to perfect condition.

I get that they have kids and so must buy new clothes more often, but if you buy designer brands for your kid that's the problem.

It's instructive to take the "What's left over" amount ($7,300) and add back all the things which are actually savings (401k, ~half of the mortgage, student loans): $47,600. This couple has a national household median income (pre-tax!) worth of money left over after their already ridiculous expenditures.

They should just stick the $7,300 into an "Other savings" line item and proclaim themselves to be living literally paycheck-to-paycheck.

People who think it's OK to spend every dime that comes in. They've bought into the recent concept that they deserve everything they want and more... then when shit happens... it's a damn hard lesson.

I can genuinely see that anybody could 'struggle' anywhere, once you consider living costs and the miscellaneous monthly payments adult life insidiously inflicts upon you.

Whilst income gradually rises, your corresponding monthly outgoings seem OK - until the income dries up (I've just watched the excellent NoClip documentary on the implosion of Telltale games in Marin County).

What I never quite grasp is why "Silicon Valley" job is still seen as a premium, rather than a massive risk.

The sole benefit I can see is that you can flit between jobs and build up your income - but as your income goes up, so does your expenditure/exposure.

I know there are other 'hubs' emerging that are cheaper - but they always seem to be 'emerging'

Is the issue the 'gambler's-dilemma'

or are you on average better off in Silicon Valley

or what?

I don't think CNBC is trying to drive a narrative here, but I do imagine that they're getting ReallyGoodEngagement™ out of articles like this since they tend to inspire immediate outrage and incredulity.

I took a look at the article they're sourcing, and that article actually has mentioned the counterpoints it expects to see about the various line items and has an argument about why they think it's reasonable that it's on there. I don't entirely agree with it, but I think the article is more nuanced than the bloomberg article suggests by just including the chart without any commentary from the article.

130k supporting a spouse and living in manhattan, and even eating out constantly, is more than enough to save a ton of money per month. 500k and struggling is ridiculous.

So after daycare a couple making $0.5M/yr would "only" have $423,000 left to work with. What does rent cost? A 6 bedroom house can be rented for $11,500 a month [1]. So after rent and daycare the family has $285,000 to work with. Still very very far from struggling.

And that's giving each child their own bedroom and saving one for guests! I grew up with me and two siblings all in the same bedroom. (And honestly, it was alright, I'm probably better for it, and we definitely weren't poor by any measure. So, the figures above should be read as "if we spoil the children", IMO.)

A thing I think is funny is that so many people feel like their kids "need" their own bedroom, then as soon as college rolls around, "dorm life" is completely fine where they have one or more roommates living in a space that is often smaller than what their bedroom back home was.

For married couple you'll still be looking at 320,000 in post-tax income at least - probably more if you have 4 kids. The rent is an over-estimate (6 bedroom house in central SF) and can easily be reduced.

Anyone living in a high COL city with multiple kids should look into importing an au pair.

$2k a month would really help the au pair and her family back home and save the family potentially hundreds of dollars a month

I know multiple au pairs living in the tri state area (mostly NYC). They seem to love the arrangement and send a ton of money back home, earn college degrees here, etc. Honestly outside of the fact they need to acquire a visa I'm not sure how this is different from having a nanny (au pair make similar pay this isn't a means to rip someone off from what I know)

Uh, pretty sure the OP is not envisioning enslaving someone. And the compensation for the au pair includes a place to live and (not sure about this) food.

He said you ought to import a person like you would import an orange and specifically said it would be ok to pay them a substandard wage as it would still be a good deal to them so they could send money home for their family.

One doesn't acquire the services of mexican's to pick your fruit merely because they work hard. You do so because they will work hard for less.

Literally the only reason to bring in someone from out of country which is implicitly a larger effort is because you have implicit leverage over that person and can use that leverage to extract more work for less money.

Further the broader context was meeting budgetary constraints.

In brief he said that in order to save money you ought to bring someone in from out of country so that you can use your leverage over them to get more work for less money while ignoring your fellow Americans looking for work because they expect things like benefits and fair pay which cost money.

It's not "leverage" it's about different expectations. You're not hiring professional childminders, the goal is to have someone come and live with you and be more like part of the family. You give them a room, I would expect food, and also pay them. Since in the US you need to go through an agency I don't think it would be a great deal of work.

> ignoring your fellow Americans looking for work because they expect things like benefits and fair pay which cost money.

Almost a quarter are from Germany. Most European countries do not consider America to be somewhere with many employee benefits.

Is $24,000 after room and board an unfair wage? What's the cost of a room in NYC?

> He said you ought to import a person like you would import an orange

It's awkward phrasing, but you don't know that they meant to compare people to commodities. Lots of people on this site do not speak English as their native language.

> Literally the only reason to bring in someone from out of country which is implicitly a larger effort is because you have implicit leverage over that person and can use that leverage to extract more work for less money.

They don't work for less because you have leverage over them. They work for less because they are not permanent residents of the U.S. and their cost of living is calibrated to their own country, which is typically less developed than the U.S.

But that's if they work for less. The price OP quoted was $2k/month. If you add on $500 in free housing, it works out to the same annual compensation as the $15/hour you cited (assuming 2000 hours/year @ $15/hour). And, FWIW, when I've looked into an au pair in the past, $2k seemed like the lower end of what they cost.

I have second hand exposure to some of this mentality... and I believe a lot of the concern from individuals comes from being entirely of social cultural upbringing where under seven figures is totally inappropriate/failing . .

Sure it will. That's a $1.2M house with 20% down. There are plenty of 2-3 bedroom 1200-1500sq ft houses around here in that range. Sure, it would be an average school district and maybe have a bit of a commute, but you can find stuff in that range for sure.

It would be $200K, but 20% is a pretty standard down payment. Yes, it would take a while to save up that much, which is why housing around here isn't affordable, but it's also pretty standard.

What does this have to do with the article about the couple living in NYC feeling average on 500k a year? In another separate market, in another region in the country... they'd pay more? OK.

Are you really sure about that? 60 000$ mortgage payment is probably more than 1 million in loan, and the property value can be double the loan (appreciation since they bought + initial payment outside of the loan). I don't exactly know the prices of houses but I guess 2 million dollar should buy you a house?

From another article with more details on this couple: "$5,000 a month in mortgage expense bought this family a ~$1,500,000, 3/2, 1,700 sqft apartment in Brooklyn a couple years ago."

My wife & I are raising 2 children in Berlin (a major world city) & earn a lot less than $500k while not struggling at all (in fact I save about 1/3 of my net pay even after deductions for both private and public retirement funds).

Sending your kids to private schools is hardly a must, especially if you live in at least a middle-class neighborhood (which I assume you do on a $500k income).

The way the United States provides schooling free of charge from age 4 to age 18, and expects families to pay massive tuition bills before and after, does make parenting expensive at times— especially for young families starting out.

$500,000 in income is, of course, enough money to pay even expensive bills, being well into the top 1% of family incomes.

People pay for private k-12 because there's a perception of the public schools being awful (and it may be true depending on the area). But if you live in a nice area with a well-funded school district, paying for private school is just ego. You won't get much of a difference in learning outcomes

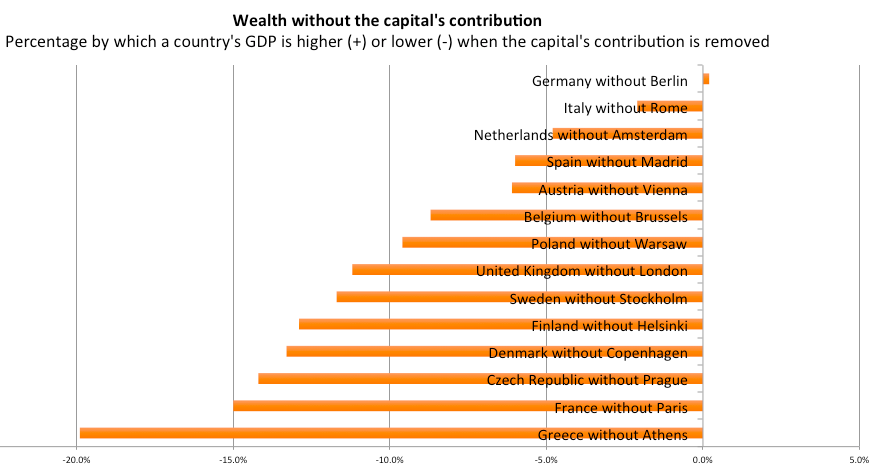

No. In fact not at all. It is one of the only capital cities in europe that is a cash drain on the nation it resides in. It is in no way a "major world city". It is not a business centre, a financial centre or a cultural centre. It is not even the most interesting or beautiful city in Germany,

Europe mostly has a much better school system with predictable outcomes that can't be achieved in much of America. The reasons for which are for another debate

Not that you don't have a point of some kind, but you are certainly ill informed about how the world works, and your place in it.

The Institute for Urban Strategies at The Mori Memorial Foundation in Tokyo issued a comprehensive study of global cities in 2018. They are ranked based on six categories: economy, research and development, cultural interaction, livability, environment, and accessibility, with 70 individual indicators among them. The top ten world cities are also ranked by subjective categories including manager, researcher, artist, visitor and resident.[13]

Global Power City top 10: 1. London, 2. New York City, 3. Tokyo, 4. Paris, 5. Singapore, 6. Amsterdam, 7. Seoul, 8. Berlin, 9. Hong Kong, 10. Sydney.

London added the entire population of Berlin in the last 20 years or less. Berlin gets on that list because of the nation state it resides in having significant world status and economic output, and not because Berlin is of any presence in the world.

I mean, this very linked article lays out the finances of some people who are doing just that and it appears to be the result of some very expensive personal choices rather than a fact of life.

My point is that this is not the case. When you take out high Federal and State taxes, high rents, tuition, etc., it's about equivalent to $80K/year income without kids. Seriously.

Holy smokes, with those kinds of expenses, you might have to hang on to that BMW 5 series a few more years before replacing it. I don't know how people are supposed to get by these days.

{kind=link}

https://en.wikipedia.org/wiki/The_Millionaire_Next_Door

"Their findings, that millionaires are disproportionately clustered in middle-class and blue collar neighborhoods and not in more affluent or white-collar communities, came as a surprise to the authors who anticipated the contrary."

It really opened my eyes to the fact that most people I think are rich are actually not rich, just extremely completely in debt.

"The authors make a distinction between the 'Balance Sheet Affluent' (those with actual wealth, or high-net-worth) and the 'Income Affluent' (those with a high income, but little actual wealth, or low net-worth)."