VCs aren't directly funded by debt. They generally receive funding from accredited investors, and accredited investors are as a rule wealthy. Now when you are wealthy you make money off your money (through traditional means stocks/derivatives/etc...) but you want to get even more wealthy and have access to special discounted loan rates through things like guaranteed loans. So you go to the bank and say here's some of my books over at Schwab and you can see there's 200M there and it's earning 10% a year on average. Now I want to put 50M into a VC firm so I can really leverage this shit up and make even more money, but I don't want to lose that 10% on the 50M and besides that the tax bill of I cash that position man...

And so the banker is like, but of course Mr Rich Dude here's a line of credit for that 50M at a low low rate of 2% since we have so much money to lend and you can keep making the now 8% interest profits by having your cake and eating it too. And if you're 200M account starts to dip too low that you might be at risk of not being able to pay us back you can always line up some more collateral or we'll margin call and collect that 50M you owe us.

Now sorry I got a bit long winded but that's really the gist of what happens, so yes indirectly VCs are largely funded by debt. And in times like these a lot of that collateral is losing value which is increasing the risk of the debt being collected, this is coupled with rising interest rates which then in turn reduces the potential reward for leveraging yourself up so much. It all becomes a vicious cycle.

Correct. Even the worlds richest man can't buy an internet company without going into debt (or crashing the stock which their "richness" is derived from)

In the U.S at least, holding cash is considered the worst thing to do if you have wealth. Which then leads people to use debt

Although Warren Buffet isn’t the richest, he surely can buy things with cash. In his last annual report, Berkshire reported 33 trillion in cash if I remember correctly. They didn’t find anything interesting to buy for a fair price so then they’ll just sit on their hands.

33 trillion would be more than the current US debt. It'd be more than 10 times the market cap of the most valued company. It'd be more than the combined market cap of the 100 most valued companies globally (seems to be at around 32 trillion for all of them).

The tl;dr is that humanity has at least an 80,000 year history of goods which are fungible, collectible, portable, scarce, and made to an exact standard, traded between people who may not speak the same language for any other sort of trade good. The familiar example is wampum, but the practice predates the colonization of the Americas by many multiples.

Debt is where state money comes from. But shell and hunk money is where states got it from, and the systems coexisted into the late 19th century.

> Is this just people being risk averse right now?

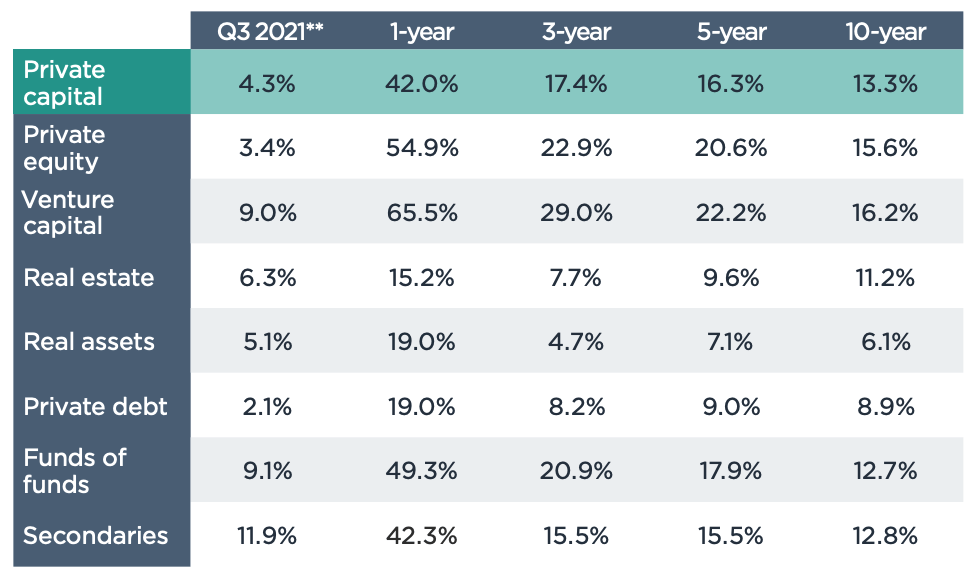

VC historically yielded 12 to 18% [1]. There is a lot of variance in those figures, with the crypto + Clubhouse guys coming in below ten, savvier funds still posting 30%+ and SoftBank + Tiger losing money.

So when a bond is yielding 5 pts [2] above the 10-Treasury’s 2.75% [3], more people will chose 7 or 8% with the guarantee of the issuer’s assets over maybe twenty maybe zilch.

There is only $2 trillion "real money", all the other money in circulation is debt. You can search for the definition of M0/M1/M2 money for more detailed explanation.

> at some point in their process they borrow money

I would be somewhat careful with such claims.

As an investor who has money available, you have two options (in this example) where none involve borrowing money:

a) invest in some startups

b) lend this money to other entities

Increased market interest rates mean that b) becomes more attractive. In other words: the startups that you invest in for a) have to be much more promising than in a market environment with lower interest rates. This means less investing in startups.

A VC fund will only get money if the risk-adjusted rate of return is greater than the rate of interest; otherwise backers of the VC fund invest their money elsewhere.

This means that VC have to become more selective with respect to the startups that they invest in, as I described.

{kind=link}

And so the banker is like, but of course Mr Rich Dude here's a line of credit for that 50M at a low low rate of 2% since we have so much money to lend and you can keep making the now 8% interest profits by having your cake and eating it too. And if you're 200M account starts to dip too low that you might be at risk of not being able to pay us back you can always line up some more collateral or we'll margin call and collect that 50M you owe us.

Now sorry I got a bit long winded but that's really the gist of what happens, so yes indirectly VCs are largely funded by debt. And in times like these a lot of that collateral is losing value which is increasing the risk of the debt being collected, this is coupled with rising interest rates which then in turn reduces the potential reward for leveraging yourself up so much. It all becomes a vicious cycle.