Ah, my information was bad. The study you originally cited specifically mentions CPI-U as the measure they were using.

I assure you I wasn't lying, and thank you for the correction. (perhaps consider not jumping straight to the lying accusation in the future).

There's still a conversation about housing taking up an increasing share of the pie that doesn't exactly shine through in that top line number, but no point in belaboring it.

> Ah, my information was bad. The study you originally cited specifically mentions CPI-U as the measure they were using.

well the BLS publishes a bunch of CPI numbers, but "the" CPI is just CPI-U. The others are even more specific (eg. CPI-W for clerical workers or CPI for the elderly)

>There's still a conversation about housing taking up an increasing share of the pie that doesn't exactly shine through in that top line number, but no point in belaboring it.

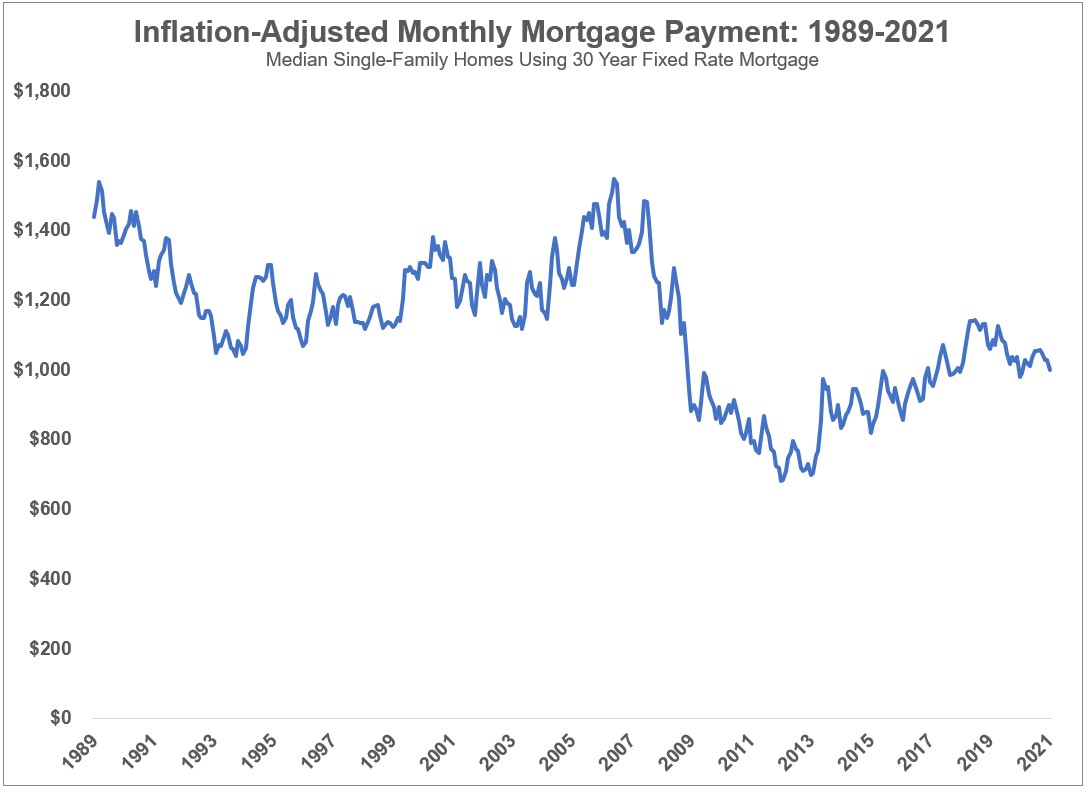

The rise in housing prices has mostly been canceled out (or caused by?) low interest rates. After you adjust for interest rate and inflation, the monthly payment for a house (ie. the price you actually pay) has actually gone down from the 90s.

> The rise in housing prices has mostly been canceled out (or caused by?) low interest rates. After you adjust for interest rate and inflation, the monthly payment for a house (ie. the price you actually pay) has actually gone down from the 90s.

Only if you ignore the tax side of things, housing interest payments are deductible where principal payments aren’t. That ends up having a huge impact when inflation and interest rates drop. It’s not uncommon for mortgages to be less affordable over time. A bump in interest rates without could really mess things up.

> That ends up having a huge impact when inflation and interest rates drop.

How so? The chart in question is for 30 year fixed rate mortgages. You're going to be making the same payment every month regardless of what direction interest rates move.

The mortgage income tax deduction means paying interest comes at a discount, paying principal doesn’t so the effective nominal payment increases over time. However, when inflation is high after 10 years the mortgage becomes trivial to pay. That dramatically increases housing affordability over a lifetime. Making a stretch purchase becomes reasonable, but if inflation is very low making the same nominal payment becomes less affordable every month.

Worse insurance and property taxes are indexed to value and don’t care about inflation. Further people can’t make the same down payment when property values increase. Identical down payments at different interest rates don’t lower monthly payments equally, and at ultra low interest rates their not even a good investment.

Housing is not included in the CPI. The housing figure is Owner's Equivalent Rent. They survey owners and ask them what they think that they could rent their home for.

They do include actual rent costs, but the weighting for rent costs has 1/3 of the weighting of Owner's Equivalent Rent. The CPI-U provides an tiny weighting of rent compared to the real rent costs for anyone who is actually renting.

{kind=link}

Yes, that's implied. If you get to choose your basket you can make inflation seem arbitrarily high/low.

>Housing, education and financial products including health insurance are not included in CPI measures -- https://www.bls.gov/opub/ted/2021/consumer-price-index-up-4-...

Why would you lie like that?

https://www.bls.gov/cpi/tables/relative-importance/2020.htm

Housing: 42.385% of CPI-U

Education: 3.033% of CPI-U

"financial products" (whatever that means, the closest I could find is "Financial services"): 0.229 of CPI-U

health insurance: 1.209% of CPI-U