I think the 40% number is the point of contention. The highest tax bracket for 2019 is 37%, and that's a marginal rate, so no one is going to be paying 37% of ALL of their income. More likely it'll be in the range of 20-25% of all income.

It's about 38% last year on that gross, as I noted elsewhere (including FICA and state). But assuming no 401(k) or match isn't realistic either so it's actually lower.

I'm not really sure why you keep pushing back on all of this. It's just how the math works.

The short version is, if you make $300k year if you are careful with the money you can have 1 million in savings in (conservatively) 6-8 years just by doing the obvious things, assuming reasonably similar market conditions.

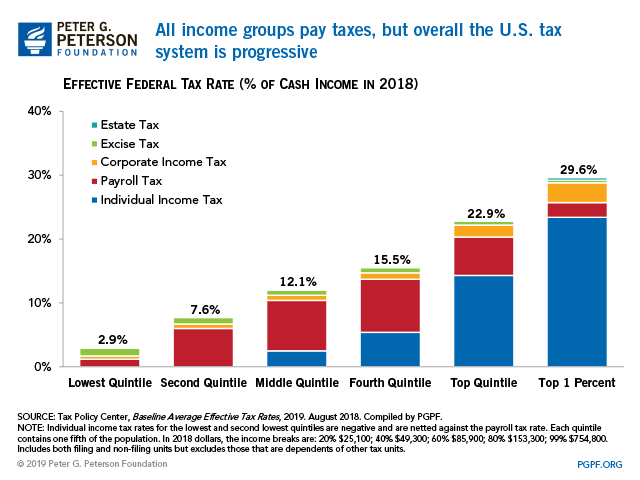

On average, the top quintile of earners pay 22.9% effective federal rate [1]. Take a look at your effective rates for 2019, I bet you pay less as a percent than you think.

{kind=link}

A FANG developer in London has even more opportunities

Max out your pension (Tax relief at 40%) plus presumably an employer match around 5-8%

Put £20k a year into a Stocks and Shares ISA - which puts that beyond tax for income and CGT (apart from stamp duty on share purchases)

Put £30k into premium bonds and than start thinking about VCT's and EIS

This is ignoring any shares scheme you are in